Mortgage Sales Funnel: How Loan Officers Build a Pipeline That Actually Converts

By Will Rapuano | Velocity Builders|

Most loan officers do not need more leads.

They need a mortgage sales funnel that stops wasting the leads they already paid for.

That distinction matters because the average lender's marketing problem is rarely top-of-funnel only. The real breakdown usually happens in the handoff between traffic, lead capture, speed-to-lead, qualification, nurture, and appointment setting. A campaign can produce clicks. A landing page can collect forms. A CRM can hold contacts. None of that guarantees pipeline.

A working mortgage sales funnel is the system that moves a prospect from first interest to funded loan with as little friction and leakage as possible.

If you are buying leads, running ads, sponsoring Realtor relationships, posting market updates, or sending traffic to your website without a defined funnel, you are not scaling. You are feeding a bucket with holes in it.

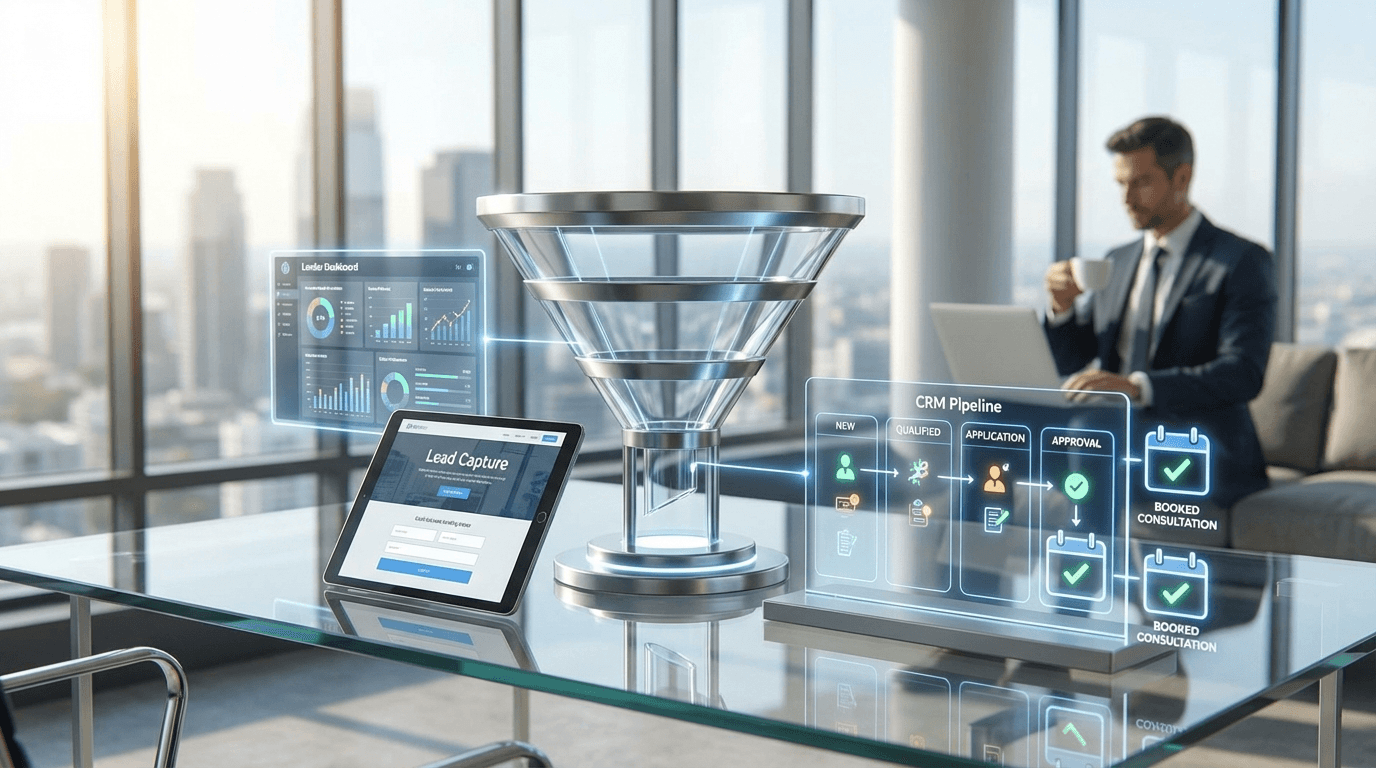

What a mortgage sales funnel actually is

A mortgage sales funnel is the sequence of pages, offers, automations, and follow-up actions that turns an unknown visitor into a booked conversation and, eventually, a funded borrower.

For a loan officer or mortgage team, that usually means six core stages:

- Traffic generation

- Lead capture

- Immediate follow-up

- Qualification

- Appointment or application start

- Ongoing nurture until the borrower is ready

Most lenders understand those stages in theory. Where they struggle is turning them into an operating system. Too many funnels are built as isolated tactics. The ad team runs campaigns. The website collects leads. The CRM sits in the background. The loan officer follows up when they can. That is not a funnel. That is disconnected activity.

A real funnel makes each stage support the next one.

The difference between lead generation and a real funnel

Lead generation gets attention. A funnel turns attention into revenue.

That is why mortgage companies often overvalue top-of-funnel performance and undervalue what happens after the form fill. They celebrate cost per lead while ignoring response time, contact rate, appointment rate, application rate, and funded volume by source.

| Area | Lead generation only | Full mortgage sales funnel |

|---|---|---|

| Goal | Get inquiries | Create appointments and funded loans |

| Landing experience | Generic page or basic form | Offer-specific page with one clear next step |

| Follow-up | Manual and inconsistent | Immediate automated response plus human outreach |

| Qualification | Happens late or ad hoc | Defined questions and routing happen early |

| CRM usage | Stores names | Triggers tasks, sequences, and segmentation |

| Measurement | Cost per lead | Contact rate, booked calls, applications, funded loans |

That table is the core issue. A lot of mortgage marketing produces names. Very little of it produces a repeatable borrower journey.

The 6 stages of a mortgage sales funnel that actually converts

1. Traffic that matches borrower intent

Not every click should go to the same destination.

Someone searching for first-time buyer financing, someone comparing refinance options, and someone asking how much house they can afford are not in the same stage of the decision cycle. Treating them the same lowers conversion before the funnel even starts.

The traffic source should map to the borrower's intent:

- Search traffic should land on pages built around the exact question or loan scenario.

- Paid traffic should connect to one offer, one audience, and one next step.

- Referral traffic should land on pages that reinforce trust and make contact easy.

- Retargeting traffic should point to a smaller commitment than a cold application ask.

This is where many lender funnels go wrong. They send every audience to the homepage or a generic "apply now" page and hope motivation does the rest.

It usually does not.

2. Lead capture with a real value exchange

A mortgage funnel works better when the prospect knows why they should raise their hand now.

That value exchange could be:

- a rate-watch or affordability consultation

- a homebuying game plan call

- a refinance savings review

- a pre-approval readiness checklist

- a local market payment breakdown

The important part is clarity. The page should answer three questions immediately:

- What is this offer?

- Who is it for?

- What happens after I submit?

If the answer is vague, conversion drops. If the form asks for too much too early, conversion drops. If the page looks like every other mortgage landing page, trust drops.

A funnel page should feel specific, useful, and easy to act on.

The middle of the funnel is where the money is won

Most lenders focus on the ad and the form. The better operators obsess over the five minutes after submission.

That is where funnel performance changes fast.

3. Immediate speed-to-lead response

A mortgage lead gets colder by the minute. If your first response depends on somebody seeing an email notification, opening a CRM later, and deciding what to say, the funnel is already losing value.

The first response layer should be automatic and immediate:

- confirmation text or email

- clear expectation for next contact

- task creation for the assigned loan officer

- source tagging inside the CRM

- routing rules if the lead belongs to a specific branch, market, or campaign

That does not replace human contact. It protects the gap before human contact happens.

4. Qualification before the salesperson improvises

A high-performing mortgage sales funnel does not make every lead start from zero in a live conversation.

Qualification should begin before the call. That can happen through form fields, campaign segmentation, landing page intent, or a short intake sequence. The goal is not to create friction for the sake of it. The goal is to help the team prioritize and personalize outreach.

Useful qualification signals include:

- purchase versus refinance intent

- timeline

- estimated credit or readiness level

- self-employed versus W-2 complexity

- property type

- location or state served

When those signals are captured early, your team can follow up with context instead of generic scripts.

5. Appointment and application progression

A lot of mortgage funnels stall because the next step is unclear.

The prospect filled out a form. Now what?

A strong funnel moves them toward one defined action:

- book a consultation

- start pre-approval

- upload documents

- complete a payment review

- schedule a refinance analysis

Too many choices create drag. Too little explanation creates hesitation. The page, the follow-up messages, and the loan officer's outreach should all reinforce the same next step.

Why most mortgage funnels fail

The common failure pattern is not mysterious. It is operational.

Here is what usually breaks:

Generic landing pages

When every campaign points to the same page, the message-match disappears. Borrowers feel like they landed in a template, not a solution built for their situation.

Slow follow-up

A funnel cannot rely on memory and inbox habits. If the first real response happens hours later, contact rates suffer.

Weak CRM structure

If the CRM is not tagging source, intent, stage, and next action, it becomes a storage tool instead of a conversion tool. That is one reason teams eventually start shopping for new software when the actual problem is workflow design.

No nurture path

Not every borrower is ready today. Without email, text, and remarketing layers built around borrower timing, the funnel only works for the hottest leads and loses the rest.

No source-to-close measurement

If you cannot tell which channels create booked calls, applications, and funded loans, budget decisions turn into guesswork.

What a high-performing funnel looks like in practice

The best mortgage sales funnels are not always complicated. They are disciplined.

A practical structure often looks like this:

Top of funnel

- Paid search or local SEO content

- Offer-specific landing page

- One strong CTA

Middle of funnel

- CRM tagging by source and borrower type

- Immediate text and email acknowledgment

- Task creation for call follow-up

- Short nurture sequence if no response

Bottom of funnel

- Appointment booking or application start

- Reminder sequences

- Document collection support

- Longer-term nurture for undecided leads

| Funnel stage | What the borrower experiences | What the team needs behind the scenes |

|---|---|---|

| Awareness | Ad, search result, referral page | Message matched to one audience and offer |

| Conversion | Short form or booking page | Tracking, tags, and source attribution |

| Response | Instant text/email confirmation | Automated workflow plus owner assignment |

| Qualification | Relevant questions and next-step guidance | Segmentation and call priority logic |

| Appointment | Booking link or application prompt | Reminders, status tracking, and accountability |

| Nurture | Follow-up over days or weeks | Automated campaigns tied to intent and timing |

That is the system view most lenders skip. They buy software and traffic before deciding how the handoffs should work.

Your website matters more than most mortgage teams think

A mortgage sales funnel usually underperforms because the website is treated like branding collateral instead of infrastructure.

Your website should not simply explain that you offer home loans. It should:

- give each audience a clear path

- support specific offers and landing pages

- build trust quickly

- make contact easy on mobile

- integrate cleanly with your CRM and follow-up system

That is why mortgage growth conversations almost always come back to site architecture and conversion design. If the site is slow, generic, hard to navigate, or disconnected from automation, every traffic source works harder than it should.

For a deeper look at that part of the system, see Mortgage Broker Website Design: What Separates a Brochure Site From a Lead Machine.

CRM and automation are not optional in a modern lender funnel

If one loan officer can personally manage every lead by memory, the funnel is too small to scale.

A modern mortgage sales funnel needs automation because borrower intent is uneven. Some people are ready this week. Some are six months out. Some need education. Some need a faster human response. A CRM should help sort that reality instead of burying it.

At minimum, your funnel should automate:

- new lead acknowledgment

- lead assignment

- reminder tasks

- non-response follow-up

- long-term nurture by intent type

- source reporting

This is where implementation beats software-shopping. The platform matters less than whether the workflow is built and actually used.

The KPIs that tell you whether your mortgage funnel is healthy

If you only track form fills, you are missing the point.

A mortgage sales funnel should be measured by movement through the funnel, not just activity at the top.

The most useful metrics are:

- landing page conversion rate

- speed to lead

- contact rate

- appointment rate

- application start rate

- funded loan rate by source

- cost per funded loan

Those numbers reveal where the bottleneck lives. A low landing-page conversion rate points to message or page issues. A poor contact rate points to follow-up speed or channel mismatch. A weak appointment rate usually points to poor qualification or a weak offer. A low funded-loan rate can expose nurture gaps, poor lead quality, or sales-process issues.

Once those metrics are visible, improvement stops being theoretical.

How to improve a mortgage sales funnel without rebuilding everything

Most lenders do not need a total reset. They need to tighten the system in order.

Start here:

- Audit every traffic source and where it lands.

- Remove generic destination pages for your most important campaigns.

- Define one immediate response workflow inside the CRM.

- Create one nurture sequence for leads who do not book right away.

- Measure booked calls and funded loans by source for the next 90 days.

That process will tell you very quickly whether the main problem is traffic quality, conversion design, follow-up execution, or offer clarity.

Once that is visible, scaling gets safer.

The strategic takeaway

A mortgage sales funnel is not a page. It is not a form. It is not one automation. It is the full system that connects borrower intent to follow-up and follow-up to funded business.

That is why so many lender marketing programs feel busy but underperform. They are running tactics without a funnel architecture underneath them.

The lenders who win in the next few years will not just be the ones buying more leads. They will be the ones with cleaner websites, faster response systems, better CRM execution, tighter offer-to-page matching, and clearer measurement from click to close.

That is the real opportunity. Not more noise. More conversion.

Velocity Builders helps real estate agents, lenders, and brokerages build websites and marketing systems that generate and convert leads automatically.

Will Rapuano

Founder, Velocity Builders LLC. Business Development Officer at Pruitt Title. Helping real estate agents and loan officers scale with better marketing systems.

Book a 20-Minute Growth Blueprint

See where your lead handoff and follow-up are leaking deals, then fix the right things first.

Book a 20-Minute Growth Blueprint